Mars Ice Cream Case

Mars ice cream’s strategy:

The strategies adopted by Mars to launch its ice cream products were the following:

-They used high-quality ingredients, such as real cream and real chocolate.

-They established a new premium-price category in the market place.

-They used significant advertising support across Europe.

-They attempted to negotiate distribution agreements with companies that were in second or third position in various national markets across Europe

-They considered freezer distribution as part of its business strategy.

The first four don´t need much explication, they used high-quality ingredients and they established a new premium-price category trying to differentiate themselves of its competitors to get more customers, they used a lot of advertisements trying to be more known across Europe and they negotiated agreements with companies that were in second or third position in its markets because of the difficulty to negotiate with the first.

However, regarding to the freezer distribution, we could say that they had excellent relationships with the grocery trade which helped them to reduce freezer distribution problem, but ice cream distribution to retail outlets involves high costs because the need for frozen storage and vehicle transport, so they had to invested considerable effort in this part of the business regarding: the low unit cost of the items carried, the small drop sizes of orders to non-supermarket outlets and the related difficulty of making up economic loads within a sufficiently compact geographic area.

Future profits from its ice cream operations:

Once we have realized which are the Mars company strategies and we understand these better we can analyze them and find the reasons because of they are not going well.

In my opinion if they maintain this strategy they don´t make significant profits in the future, so we are going to identify which are the things that they are doing wrong and what they should change to make profits in the future.

There are two main strategies they aren´t doing well:

-First of all I would like to say that if you use high-quality ingredients and you establish a new premium-price category, maybe you don´t have to sell your products in typical supermarkets and you have to focus in specialized supermarkets and stores which focus on that specific market segment, so in my opinion this could be a solution and the other will be changing its strategy and selling its products in all kind of supermarkets, but not using high-quality ingredients and not establishing a new premium-price category. So Mars Ice Cream has to define its audience better and to follow one strategy or the other. They have to select better its audience or on the other hand if they decide to expand its audience and to sell its products in all kind of supermarkets, also they could diversify their products with dessert ice creams, ice creams for children or something like that.

-And the other is of course freezer distribution, as we have seen this has several problems and according to that Mars has considered that as a very important part of its business, but even on that they aren´t doing well. The goal has to be to minimize all these several problems and a solution for that could be to open new factories closer to their consumption zones, having only one factory in France this problem can´t be solve or at least is much more complicated. Also if they change its strategy of high-quality ingredients and they expand its audience, they could diversify more, expand its product offering and solve freezer distribution problems transporting more products and minimizing its costs.

Comentarios desactivados en Mars Ice Cream Case /

04 Dic 2011

por

Alberto Rengel Bueno

MERME /

MERME /

Strategy: Mars ice cream case

After analyzing the business case, here are my answers to the questions:

How would you resume the strategies adopted by Mars to launch its ice cream products?

Mars´ main strategy was to use high-quality ingredients in their products. They made important advertisements all over Europe in order to promote their products and their high quality. Their strategy also included a higher price than the one for similar products; this is a way to differentiate Mars from the other products, because this price reflects that Mars´ quality is higher. When consumers see the price, they associate higher prices with higher quality.

It is also interesting the fact that Mars products look the same all over Europe, so consumers can buy them without any doubt when they are travelling or when they change their home. Same product, same appearence.

Mars also spent a lot of efforts in freezer distribution, but this strategy worked much worse than for other well established companies, like Nestle and Unilever. These two companies offered free freezers to shops with the condition that these freezers would only be used for their products. Big supermarkets didn´t need them, but it was a good strategy within small shops. Mars could not compete with this: Mars´ products were not allowed in Unilever and Nestle´s freezers plus Mars was focused in one kind of product, while the other companies were diversified. Mars had to share the freezers with dessert ice creams, children´s novelty ice creams… from other brands, because retailers needed to sell different products.

Do you think that Mars will ever make significant profits from its ice cream operations? Why? How?

In my opinion, Mars has to change its strategy in order to make profits. I don´t think the actual one is working properly, not even in the long run.

The first mistake I find is the one factory in eastern France. It could work with a smaller market, but if they want to distribute their products all over Europe, which is the case, it´s not the smartest strategy. The transportation costs are extremely high as the products need freezers. Maybe having several factories or storage places around Europe could decrease these costs. They could also share transportation costs with other small companies that will distribute their products in the same shops.

The actual strategy makes it difficult to have profits. Small shops cannot sell big amounts of Mars and, as the cost of transporting Mars to these shops is high, this is a big problem. The most efficient transport is that to big supermarkets, because they can sell bigger amounts of Mars´ products, so transportation costs are worth in these cases. Mars could focus only on big supermarkets, but small shops sell lots of snacks, so I don´t think it´s the best option. If Mars wants to sell its products in small shops and have benefits, they must change their transportation strategy. Besides sharing transportation costs, as mentioned above, they could try to reach an agreement with Unilever or Nestle in order to share their freezers, but I don´t think that these companies have a big interest in these negotiation because they are much more powerful than Mars right now.

It´s true that the high quality of the product helps to differentiate it from the other sweet snacks, but not all snacks´ consumers are searching for high quality. Anyway, the advertisement seems to work because, even with all the difficulties the product has faced, at least there were no losses. Advertisement is important to have loyal consumers searching for quality and I think they should focus on advertisement to make more people aware about the quality of their products, because each day society is demanding healthier products.

Unilever and Nestle competition is a risk. They are not selling so high quality products, their prices are lower and they are diversified. Mars has to face the fact that many people will buy cheaper snacks, caring only about the taste and price, and that diversified companies have a higher chance to succeed in small shops. Mars´ new strategy must consider all these threats in order to succeed and make profits. Mars could expand their businesses and produce dessert ice creams… several products that can be distributed and storage together and that can help to create loyal consumers, buying all these similar products from the same company, because right now, if a consumer wants a Mars ice cream bar and a dessert ice cream, the dessert ice cream would be from another brand.

To sum up, Mars should change its strategy: diversify the products, face the problem of the high distrubution costs and continue betting on the quality of its products, because is what makes them different from the ones sold by other brands and without these differentiation, they would be in a worse position.

Comentarios desactivados en Strategy: Mars ice cream case /

03 Dic 2011

por

Maria Diez Maroto

MERME /

Integración de Renovables y Diseño de Mercado Eléctrico: Es necesario implementar CRMs para asegurar el suministro eléctrico?

El artículo de EURELECTRIC: “RES Integration and Energy Market Design: Are CRMs Needed to Ensure Generation Adequacy?” aborda el tema de generation adequacy o la capacidad del sistema eléctrico de generar exactamente el consumo que demanda el mercado y cómo lograr que se desarrolle un mercado eléctrico que logre funcionar adecuadamente en todo momento, desde el punto de vista de los conceptos de diseño. Para ello introduce la interrogante de qué tan importante es la utilización de los Mecanismos de Remuneración de la Capacidad (CRM por sus siglas en inglés) para lograr el acometido antes mencionado.

Se describe en el texto cómo a pesar de la necesidad y relevancia de la introducción de las EERR en los sistemas eléctricos, la instalación en gran escala de centrales renovables, combinado con su prioridad de despecho e intermitencia intrínseca, está reduciendo el factor de carga de las plantas de generación eléctrica convencionales debilitando su habilidad para recuperar sus costos fijos y encaminándolas a su parada definitiva. De manera similar, posibles inversores de nueva capacidad convencional pueden enfrentar una creciente incertidumbre, debilitando las inversiones en estas tecnologías. A pesar de que las plantas más ineficientes y contaminantes sí deberían reemplazarse, lo cierto es que esta situación también afecta a la nueva centrales más eficientes y limpias que deseen instalarse.

Esta situación es posible entenderla como un grave problema para los sistemas eléctricos debido a la importancia que tienen estas plantas para administrarle al mismo los niveles suficientes de firmeza para hacerlo operar de forma segura. Esto se entiende como las propiedades que tienen las centrales convencionales para ofrecer capacidad o reservas que logren cubrir picos de demanda, imprevistos, imbalances del sistema y la misma intermitencia de las energías renovables. Este último punto brinda la clave para entender cómo este problema afecta a las renovables y su integración al sistema. Básicamente, las centrales convencionales y concretamente las más flexibles, son las que brindan un complemento a las EERR al cubrir su intermitencia y demandando de ellas características técnicas cada vez más desafiantes cómo rampas de subida más pronunciadas, menores valores carga mínimos estable, entre otros.

Este problema se agrava aún más en los países donde el diseño de los mercados de sólo-energía no son adecuados e impiden la correcta interacción entre la generación y la demanda. En concreto, distorsiones como: regulación del precio final, restricciones en la operación de plantas, Price caps, falta de interconexiones con otros países, falta de participación de la demanda en el mercado, competencia de las renovables en el mercado, son los posibles contribuyentes a un déficit en los ingresos que estas centrales convencionales están percibiendo y pueden llegar a amenazar la seguridad de generación .

Para corregir estas distorsiones que en mayor o menor medida están ocurriendo en los países europeos se proponen los CRMs. Mediante estos mecanismos la intención es ayudar a los generadores para que recuperen la parte de sus costes que no están percibiendo por la ineficiencia y distorsiones del mercado de energía. Se pretende entonces remunerar por capacidad (MW) instalada y disponible para el sistema, y no sólo por energía brindada (MWh), mediante diferentes mecanismos.

La gran interrogante surge al preguntarse cuándo es más adecuado introducir estos mecanismos. EURELECTRIC plantea tres características básicas, que los países necesitan valorar para saber si es necesario introducir CRMs:

Poca o despreciable participación e interacción de la demanda en casación del precio.

Falta de capacidad de interconexión con otros mercados.

Presencia de significantes distorsiones regulatorias u operacionales del mercado (Price caps, regulación restrictiva sobre la mezcla de plantas de generación).

En estos casos, se propone alguno de los siguientes mecanismos:

Capacity payment (CP): se le paga un fijo a todos los generadores por su capacidad disponible.

Tender for a targeted resource (TTR): se le paga a los recursos por su disponibilidad para hacer frente a las variaciones en la demanda, mediante una licitación.

Capacity obligation/ Ticket (CO): Los productores están obligados a tener contratada una capacidad de reserva, en función de su perfil de producción.

Capacity Auction (CA): La capacidad es determinada centralmente, con años de anticipación, se licita el precio y se le paga a todos los recursos que se presenten a la licitiación, tanto existentes como nuevos.

Reliability Option (RO): Es un modelo similar al anterior, pero en un mercado financiero, no real. Los generadores deben estar disponibles para producir una vez que el precio de la electricidad superó cierto valor.

Es importante resaltar que se hace inca pie a que los CRMs deben ser retirados inmediatamente se logre asegurar la seguridad de generación del sistema.

Análisis del Caso Español

España brinda un panorama con muchas fortalezas, pero al mismo tiempo bastantes debilidades que hacen necesario la evaluación de las CRMs como una posible solución a hacer un mercado eléctrico más competitivo, más justo, pero sobre todo que brinde un mayor generation adequacy.

En primer lugar, debido a la alta penetración en el mercado eléctrico de las Energías Renovables, un mecanismo que asegure el suministro debido a las intermitencias de las mismas, es necesario.

Actualmente, España tiene un mecanismo de CRM en su regulación secundaria y terciaria, en el cual se la paga a los productores por su capacidad de bajar o subir la producción de energía. El precio de dicha potencia es pagado a valores de mercado: el Operador del Sistema (Red Eléctrica) determina cuál es la capacidad necesaria, y los productores envían sus ofertas.

A partir del 2007, España ha implementado mecanismos de pago por capacidad para el mediano y largo plazo.

En el mediano plazo, el OS contrata bilateralmente con el productor una capacidad por un plazo menor a un año. Dicho contrato debe ser revisado por la CNE y aprobado por la Secretaría General de la Energía.

En el largo plazo, considerando la necesidad de promover nuevas centrales para garantizar la potencia necesaria, el OS determina una cierta potencia a instalar, que pueden ser subastada por la Secretaría General de la Energía.

La efectividad de estos mecanismos, sobre todo en el largo plazo, deberá ser evaluada y revisada. Para evitar tener que recurrir a estos mecanismos, se deben implementar cambios y mejoras en el sistema. Los price caps, deberían considerarse eliminarlos poco a poco o al menos mantenerlos siempre en un valor lo suficientemente alto cómo para que no afecten la interacción normal entre la demanda y la oferta. El aumento de capacidad en la interconexión eléctrica con Francia debe ser una prioridad a corto plazo.

Hasta el momento, España ha admitido una alta penetración de las EERR en forma adecuada, sin colapsos en el sistema. Los mecanismos utilizados han permitido estos porcentajes, y deberán seguir utilizándose y mejorando en forma ordenada, para permitir una mayor diversificación de la base eléctrica española y sobre todo asegurar siempre el suministro.

Autores:

Ricardo Garro/María Abella/Carlos Aparicio/Federico Camino. Grupo 2

Comentarios desactivados en Integración de Renovables y Diseño de Mercado Eléctrico: Es necesario implementar CRMs para asegurar el suministro eléctrico? /

02 Dic 2011

por

Ricardo Garro Ruiz

MERME /

Mars Ice Cream: Its Strategy and Future

The company Mars Ice Cream has included several strategies into its operation, some are differentiating and some others might have not being so well analyzed, but the truth is that it has certain opportunities which they are not converting into the greatest results and this can compromise its future.

1. Mars Ice Cream´s Strategy

The approach of this ice cream company to the market has been through the use of high quality ingredients to make their products. They established a premium price category in the market place. At the same time, they are using an important advertising support thorough all Europe and have established long standing relationships with grocery trade. Trying to reach even more clients, they adopted the strategy of freezer distribution.

It is clear that the company wants to differentiate from the competition by having high quality, premium products. To increase sales and attract more clients they are targeting supermarkets and small markets and even offering freezers to them.

Now, it is evident that the company is facing several problems regarding high distribution costs, small orders on non-supermarkets stores, and bad businesses with freezers.

In general, Mars Ice Cream has adopted a very similar operating strategy than its competitors. This is being very ironic because their products are different, and their market niche should not be exactly the same.

2. Future About Its Profits

After taking into account the factors detailed above we can infer that something is not going well and that probably if they don´t change their strategy, the company´s results will not have a great outcome.

On one side we have the current strategy of the company. I believe that Mars Ice Cream has not defined its “audience” or market niche correctly or at least is not acting according to it. I think that by having a specialized product they should focus in certain type of supermarkets or stores which can offer those premium products to that specific market segment only. But if what they want is to diversify their type of clients, they should also diversify their products with dessert ice creams, bulk ice cream packs or ice creams for children. For me this is one of its biggest mistakes.

Their distribution problems should also be address by changing the strategy, they should open new factories closer to their consumption zones or associate with local companies for other better distribution schemes. The freezer approach can only continue if they expand their product offering, any other way will have very little success.

To change their strategy and adapt to the current needs they should study the external factors currently affecting it, so let’s make a quick analysis of the external factors affecting the company using Porter´s 5 forces:

• Threats of New Entrants: Mars Ice Cream has good distribution contacts, high quality and specialized suppliers; but, at the same time its production its very centralized; all is branded the same and their distribution costs are high which facilitate competition. Grade: Medium.

• Substitute of products: cheaper and not premium products are stealing market; Nestle and Unileve have big market shares and have broader range of products and could easily adopt a premium product approach. Grade: High

• Suppliers Power: By using high quality products, which can be very well-known products of even bigger and few enterprises, they can influence greatly on the Mars. Grade: High.

• Buyers Power: Having premium products makes it too special or expensive for certain buyers in common stores. Grade: High.

• Rivalry Intensity: High fixed costs and high storage can increase competition. Nestle and Unilever are very important companies, best positioned than Mars and can attack whichever market niche that they want. Grade: Medium-High.

In conclusion, it is currently a difficult market and they cannot continue with the present strategy. Unless they change their current approach to the market and enhance their opportunities and strengths while diminishing their weaknesses, they will never make substantial profits.

Comentarios desactivados en Mars Ice Cream: Its Strategy and Future /

02 Dic 2011

por

Ricardo Garro Ruiz

MERME /

El porqué de los números de nuestra tarifa eléctrica

¿Cuántos de vosotros miráis la factura de la electricidad y no entendéis lo que significa? ¿Pagáis sin saber muy bien qué estáis pagando? Con este post queremos, al menos intentar, que esto no vuelva a pasar.

Desde 1998 el sector eléctrico español dejó de ser monopolista y hoy en día contamos con actividades reguladas (transporte y distribución) y actividades liberalizadas (producción y comercialización). Los consumidores finales pueden comprar su energía de diversas formas: mercados diario e intra-diario, contratos bilaterales y mediante los suministradores de último recurso (SUR).

Dado que la mayoría de hogares españoles pagamos la energía a un SUR, al precio fijado o tarifa último recurso (TUR), vamos a centrarnos en esta tarifa. La TUR entró en vigor el 1 de Julio de 2009 y tiene un precio único para todos los consumidores que es independiente de la empresa que les comercializa la energía (cualquier consumidor podrá elegir su suministrador de electricidad). Para poder acogerse a la TUR es necesario que la potencia sea menor o igual a 10 kW. Para saber más de esta tarifa, recomendamos visitar el siguiente enlace:

http://www.youtube.com/watch?v=rFv2SatDRrg

La facturación de la TUR se realiza mensualmente y se calcula cada tres meses de forma aditiva. El precio de la tarifa viene determinado por:

– Coste de adquisición de la energía: mediante subastas CESUR, realizadas para obtener de forma competitiva el precio para los clientes de la TUR. En ellas, se asignan contratos para el suministro de energía mediante una subasta de precio descendente. Al resultado de la subasta se añaden otros costes como los resultantes de la participación en los mercados spot y los pagos de capacidad y pérdidas. Esta subasta se realiza trimestralmente y el gobierno no puede intervenir en la misma.

– Tarifa de acceso: incorpora el precio correspondiente según el consumidor y está fijada por el gobierno.

– Gestión comercial: trata de reflejar el coste de los procesos de gestión y también está fijado por el gobierno.

ANALISIS DE LA FACTURA ELECTRICA

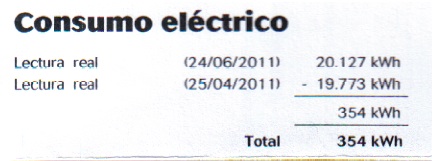

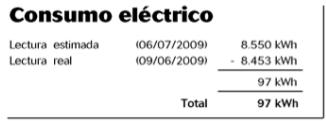

Lectura Real:

Consiste en la lectura que marca tu contador en la fecha que se indica en la figura.

Es posible, sin embargo, que uno de cada dos meses la lectura sea estimada, tal y como se muestra a continuación:

En este caso, se calcula en función de tu consumo durante ese mismo período el año anterior, por lo que nuestra recomendación es que espere a la factura con consumo real para verificar los importes cobrados en su conjunto. No obstante puede verificar si la estimación es correcta o no acudiendo a la factura del año anterior para las fechas dadas.

Como las lecturas no se realizan entre periodos exactos de 2 meses, su compañía debe calcular el consumo diario de electricidad en la factura real del año anterior y multiplicar ese consumo por los días incluidos en la factura estimada actual. Si considera que la estimación es incorrecta puede reclamar a su compañía, no obstante, cualquier desviación se corrige con el mes siguiente.

Toda esta situación de desconcierto con respecto a nuestra factura tarifaria se podría evitar con el simple hecho de efectuar la lectura de contadores de manera mensual. Sin embargo es evidente que las comercializadoras eléctricas de ultimo recurso, con el consentimiento del gobierno, no están por la labor de afrontar los gastos en contratación que ello supondría, (que por cierto, nos vendría que ni anillo al dedo como capote a los tiempos de crisis en los que estamos inmersos) ofreciéndonos actualmente algunas de ellas, eso si, la posibilidad de introducir dicha lectura manualmente vía internet al usuario correspondiente. A falta de no generar trabajo, hemos de trabajar todos los españoles en tareas que no nos conciernen.

Coste Consumo:

Este coste consiste en la multiplicación del consumo realizado durante el período de tiempo reflejado (gráfica previa de consumo) por la cantidad a la que la compañía cobra el kW. Este aspecto está regulado por Real Decreto, y el recibo también indica el número y fecha del BOE en que se fijó la cuantía de dicho concepto.

En el siguiente link, se muestran los últimos valores de precios de tarifa eléctrica publicadas en el BOE a 30 de Septiembre de 2011 (estas tarifas son fijadas semestralmente por el Ministerio). En ella vemos como los valores con respecto a los fijados en el anterior decreto del 31-03-2011 han aumentado en una proporción, que a efectos del consumidor parece ínfima, pero que desde el punto de vista del Gobierno y comercializadoras supone un más que increíble aumento de sus ingresos. Y es que no queda más remedio que estas subidas continuas en la factura ante la situación de déficit que el sector vive en la actualidad, y que será explicado en la última parte de este post.

Descuentos:

Este es un buen momento para detenerse, y explicar el porqué y lo que esconden en el fondo estos descuentos, ya que es con estos valores con los que juegan las compañías, a efecto de cautivar a posibles clientes al cambio. Cuando decidimos en grupo el objetivo a explicar en este post, uno de nosotros se puso en contacto con su padre, pidiéndole que nos enviase vía mail una de sus facturas eléctricas más recientes. Tras revisar esta brevemente, nos llamó la atención la presencia de estos descuentos, por lo que nos pusimos en contacto con él de nuevo y le preguntamos sobre ello. Su respuesta literal fué: “Pues no se muy bien a que se refieren la verdad”.

El tan diseñado engaño, radica en que las compañías por lo general te comentan que te ofrecen un 10 o 15%, como es este caso, pero no sobre que lo van aplicar, que por norma general, y como aquí se refleja, suele ser el término de potencia y no el de consumo, el cual nos supondría un beneficio mucho mayor. Además, y haciendo mayor la trampa, este nuevo contrato suele ir acompañado de un incremente en el gasto del alquiler de contadores (a punto electricidad), ya que como este caso, el pago de 12,13 €/mes parece del todo excesivo.

Término de Potencia:

Consiste en el importe fijo, que la compañía cobra con respecto a la potencia que tenemos contratada. Mayormente este valor hace referencia a la utilización de sus redes eléctricas (distribución), y es un importe que se abona siempre, incluso en el caso de no haber consumido electricidad. Para los hogares españoles, las potencias contratadas más frecuentes se sitúan entre los 3,3 y 5,5 kW, sin embargo en la actualidad, las principales comercializadoras disponen de herramientas web (endesa, iberdrola) que nos ayudan en dicho cálculo, en función de los electrodomésticos o aparatos electrónicos de los que disponemos y del uso simultáneo que hagamos de los mismos, junto con la iluminación del hogar.

Impuesto especial sobre la electricidad:

Impuesto que se recauda en España, fijado por el gobierno, para su posterior inversión en I+D+i de energías alternativas y nuevas estructuras de la red (por ejemplo, el actual desarrollo de las configuraciones “smartgrid”), para paliar la carencia por no construir nuevas centrales nucleares. Este concepto, como se refleja en el recorte de la factura, se paga sobre el consumo de la electricidad y la potencia contratada y está cifrado en un 4,864%.

A punto electricidad (ó, alquiler de equipos de medida):

Cuando el consumidor no es el propietario del contador, la distribuidora le cobra su alquiler con la misma periodicidad que su factura, cuyo coste es fijado periódicamente por el Gobierno.

IVA e IGIC:

El impuesto sobre la electricidad está a su vez gravado con el 18% de IVA, IGIC en el caso de que vivas en Canarias.

EL DEFICIT TARIFARIO

El déficit de tarifas es la diferencia entre el total recaudado por las tarifas integrales y tarifas de acceso (que fija la Administración y que pagan los consumidores por sus suministros regulados y competitivos, respectivamente) y los costes reales asociados a dichas tarifas (principalmente transporte y distribución)

Las diferencias entre la recaudación por tarifas integrales y de acceso y los costes reales de las mismas se originan básicamente de dos maneras – errores de estimación y decisiones regulatorias del Gobierno.

Sin embargo, estos errores de previsión sólo crearían un déficit coyuntural (y no estructural), siempre y cuando, la probabilidad de error al alza y a la baja fuera la misma a lo largo de los años. Los errores en sentido positivo (sobre-recaudación) compensarían los errores en sentido negativo (infra-recaudación), con lo que a largo plazo el déficit promedio tendería a ser nulo.

Existe divergencia entre los costes reales esperados y los costes “deseados” por el regulador y los Gobiernos han preferido incluir en el proceso de cálculo de las tarifas el “coste deseado” del suministro, en vez del “coste real esperado”.

Esta contención de las tarifas, sin embargo, no conlleva un menor ingreso de las empresas que realizan actividades eléctricas 1 puesto que, por imperativo legal, éstas deben ser retribuidas según su coste reconocido, cuando son actividades reguladas (redes) y según el precio que emana de los mercados mayoristas cuando son actividades liberalizadas (generación).

Esta forma de proceder por parte de los gobiernos da lugar a un déficit estructural cada vez más elevado y difícil de mantener, que tiene efectos sobre el desarrollo de la competencia en los mercados y sobre las señales económicas que reciben generadores y demanda.

A finales de 2010 se situaba el déficit por encima de los 20.000 millones de euros. De seguir en esta tendencia y si los gobiernos no ponen freno a la situación podríamos llegar a los 40.000 millones de euros en 2020.

Para evitar esta tendencia, poco a poco habrá que hacer incrementos progresivos en las tarifas hasta que lleguen a converger los ingresos con los costes. Así mismo el transporte, la distribución y las primas de régimen especial deben ser revisadas para detectar donde existe un exceso o un déficit de retribución. Esto ya sucede con las primas de régimen especial que van disminuyendo progresivamente a medida que se recupera la inversión de la instalación.

El reto es intentar que el déficit no crezca para 2013 para lo cual habrá que aumentar un 10% en estos dos años la tarifa, y a partir de ahí aumentarla con una tendencia de un 3,5%.

GRUPO 4:

Bueno Serrano, Álvaro

Diez Maroto, María

Medal Rendal, Alfonso

Comentarios desactivados en El porqué de los números de nuestra tarifa eléctrica /

01 Dic 2011

por

Alfonso Medal Rendal

MERME /

STRATEGY ASSIGNMENT AND BUSINESS CASE

As we have been analyzing in the first 3 sessions of the course, strategy is the pattern or plan that integrates an organization’s major goals, policies and action sequences into a cohesive whole. Business Strategy is concerned with an organization´s basic direction for the future: its purpose, its ambition, its resources and how it interacts with the world in which it operates. Business strategy is basically about competitive advantage, the plan that enables an organization to gain, as efficiently as possible, a sustainable edge over its competitors.

Obviously, the purpose of this course is to equip you students with the core concepts, frameworks and techniques of business strategy. The good strategist analyzes the industry environment and the internal generic conditions of its competitors in order to get conclusions about the concrete situation of his company and design all the possible ways to compete within its industry.

Since we have examined each of the different components of the business strategy and the basic tools of strategic analysis, now it is time you show me that you have understood the basic frameworks and techniques of business strategy.

The business case has been sent by mail.

Each one of you has to upload a post answering to the two case questions. If you have any doubt, don´t hesitate to contact me via e-mail.

I profit to send you a couple of very interesting and enlightening links. The first one is a debate between longtime Fortune magazine technology writer and guru David Kirkpatrick and Mark Zuckerberg, co-creator of the social networking site Facebook, of which he is Chief Executive and President:

The second one is a lecture by Dr. Patrick Dixon, a world famous and renowned author and business consultant, one of the most influential business thinkers around the world:

http://www.youtube.com/watch?v=_kZl15houUc

From Jon Icazuriaga, EOI´s teacher.

Comentarios desactivados en STRATEGY ASSIGNMENT AND BUSINESS CASE /

01 Dic 2011

por

evacurto

MERME /

Strategy:Mars in the Earth

It´s difficult to talk about a company without knowing your economic situation. Also, why it decided to follow one strategy in a particular time. In this case, the brand is Mars and its necessities of new challenge.

It´s difficult to talk about a company without knowing your economic situation. Also, why it decided to follow one strategy in a particular time. In this case, the brand is Mars and its necessities of new challenge.

Looking at percentage figures, Mars has a solid position in the European market with its chocolate bars. Apparently, Mars had enough arguments to go into a new business. High share in the market, high quality in its ingredients, well-known confectionery products and premium level inside of the snack market are some of its strengths. However, there is a point which I don´t consider positive in this kind of product. It´s the premium-price category in the market. Pricing almost near of the high end of the possible price range is used to enhance and reinforce a product´s luxury image. Consumers of this type of products believe that the high price indicates good quality. Also, you belong to an exclusive group or higher status. It makes sense in cars, clocks, clothes….but it doesn´t it whether we talk about snacks. Above all, in a market with huge competence and low prices. Kit Kat, Twist, Kinder, Huesitos are some examples with cheaper prices. These products are oriented to young people who usually don´t have much money. It´s a disadvantage in my opinion despite of its higher quality ingredients.

Mars´ strategy in distribution is looking for provisional solutions in the absence of a planification in origin. Mars is patching its lack of forecast in some aspect as logistic. A only factory in France is not enough to supply all Europe. Also, ice cream is a seasonal product with expiration date and a special way of transport and conservation. Mars didn´t see which were its barriers and its competitors. Unilever and Nestlé are larger companies with a diversified business. They can put packs of different products together thanks their diversification. In fact, they do it in supermarkets with product such as Ben&Jerry´s, Frigo, Calvé, etc…..all belonging to Unilever. Mars can´t compete with Unilever´s logistic and agreements. In spite of making some agreements with companies such as Lyons Maid or Miko. It turned out in only a provisional solution. As we could see, those companies were taken over by Nestlé and Unilever time later. Therefore, Mars didn´t get to solve its problems with frozen cabinets, transport and supply for retailers.

I guess, in the strategic plan of Mars would be the fact to make money and do a profitable business. Nevertheless, if we have in account extra costs such as transport, new logistic, freezers for retailers, new agreements, etc….benefits will be less than Mars expects. Also, Mars is already expensive enough product in itself. A priori some thing so easy as freeze the bar and put a stick involve more problems than you could see at the beginning. I think, Mars has a weak position in front of its competitors in the ice cream world. For instance, Spain is dominated by Frigo (Unilever) and Nestlé with some small competitors (low percentage of sales) such as “La menorquina” and “La polar” in some places.

Probably “Mars” ice cream would be in conditions to be absorbed by another larger company. In the text we can read that they got profits in 2000, ¿ Were so many benefits as Mars expected? I don´t think so. Benefits, yes….but not so many ones that they expect.

Comentarios desactivados en Strategy:Mars in the Earth /

01 Dic 2011

por

Jonathan Cabrero Sanchez

MERME /

Managerial skills

With this essay, I will finish the Managerial skills course. I have enjoyed and learnt a lot and I have found it very useful both to my professional career and dayle life. Let’s see the contributions I have received from the three units of the subjetc.

Effective Presentations

Nowadays, to make effective presentations is a very important issue for a good professional performance. If you want to work for a company, you will not start working unless you can sell yourself in the interview. And later you will need to keep making presentations for your managers, clients or suppliers.

Some keys like the main principles for make effective presentations or the concept of WIIFY have been very useful.

I made my first presentation in my life! And to gain experience is always a good value in order to know our strengths and weaknesses as a presenter.

Negotiation

Life is based on give and receive; the more you give the more you get. The negotiations are also based on this principles and, in most of cases, to find a balance between what you give and what you receive. So, negotiations are very deep-rooted in our lifes. We bargain with our friends for decide what can we do after class, with our parents when we were teenagers in order to decide the arrive time to home or to solve any conflict or misunderstanding. This are dayly situations but also in our professional life we will negotiate since we start working, bargaining the job conditions and later with managers, clients or suppliers.

So to know the main keys like the stages and characteristics of negotiations, and the concept of BATNA (Best Alternative To Negotiated Agreement) are very useful.

Leadership

This theme has becomen my favourite even the lack of time for assimilate all points.

The keys of motivation and the Pickle jam theory have been very inspiring.

The Manager vs Leader matter is very important and interesting because of the lack of leadership that nowadays affects the World, specially Europe and Spain.

And to finish, the Problem frame vs Solution frame question have been very important for me. I realized that often I think focusing on the problems and not on the solutions, so I waste large amounts of time asking to myself asking Why? instead of How? This behaviour decrease my motivation, so changing this I will be more effective and happier.

I find amazing how small changes in our attitudes can change even the life of a person.

And to conclude, the contribution of the teacher has been essential in order to get the messages, because the lessons have been very clear and get you hooked. And also, the atmosphere in the class has been very nice and participative.

Comentarios desactivados en Managerial skills /

30 Nov 2011

por

David Garcia

Sin categoría /

Managerial skills

With this essay, I will finish the Managerial skills course. I have enjoyed and learnt a lot and I have found it very useful both to my professional career and dayle life. Let’s see the contributions I have received from the three units of the subjetc.

Effective Presentations

Nowadays, to make effective presentations is a very important issue for a good professional performance. If you want to work for a company, you will not start working unless you can sell yourself in the interview. And later you will need to keep making presentations for your managers, clients or suppliers.

Some keys like the main principles for make effective presentations or the concept of WIIFY have been very useful.

I made my first presentation in my life! And to gain experience is always a good value in order to know our strengths and weaknesses as a presenter.

Negotiation

Life is based on give and receive; the more you give the more you get. The negotiations are also based on this principles and, in most of cases, to find a balance between what you give and what you receive. So, negotiations are very deep-rooted in our lifes. We bargain with our friends for decide what can we do after class, with our parents when we were teenagers in order to decide the arrive time to home or to solve any conflict or misunderstanding. This are dayly situations but also in our professional life we will negotiate since we start working, bargaining the job conditions and later with managers, clients or suppliers.

So to know the main keys like the stages and characteristics of negotiations, and the concept of BATNA (Best Alternative To Negotiated Agreement) are very useful.

Leadership

This theme has becomen my favourite even the lack of time for assimilate all points.

The keys of motivation and the Pickle jam theory have been very inspiring.

The Manager vs Leader matter is very important and interesting because of the lack of leadership that nowadays affects the World, specially Europe and Spain.

And to finish, the Problem frame vs Solution frame question have been very important for me. I realized that often I think focusing on the problems and not on the solutions, so I waste large amounts of time asking to myself asking Why? instead of How? This behaviour decrease my motivation, so changing this I will be more effective and happier.

I find amazing how small changes in our attitudes can change even the life of a person.

And to conclude, the contribution of the teacher has been essential in order to get the messages, because the lessons have been very clear and get you hooked. And also, the atmosphere in the class has been very nice and participative.

6 comentarios /

30 Nov 2011

por

David Garcia

Sin categoría /

Eroski financial situation

Eroski is a Spanish supermarket chain with nearly 1,000 outlets spread across Spain (excluding franchises). It is run as a worker-consumer hybrid co-operative within the Mondragon Corporation group. The establishments vary in size from the largest hypermarkets, simply named ‘Eroski’ (of which there are 75 stores, including 40 with petrol stations), down to smaller ‘Eroski Center’ stores (473, including 2 petrol stations). There are also 219 ‘Eroski City’ outlets, 234 ‘Eroski Viajes’ travel agent centres and 44 ‘Forum Sport’ sport clothing stores. The group’s total sales floor space is approximately 1,500,000 square metres.

At the end of fiscal year 2010, Eroski has obtained an increased by 17% in the Operating profit, reaching 100million €. Furthermore, Eroski has reduced their financial expenses, so there is a increased in the EBIT by 20.4 million €. Eroski repeats EBITDA, 419 million €

In order to face the crisis, the decrease of the activity and the increase of the IVA, Eroski has made an important reduction of their prices and has intensified the return of money to banks in order to reduce their financial debt.

Let’s see Eroski’s figures step by step (measured in million €):

Assets=3.432.654

Current Assets– 1.471.762

The 65% of CA comes from Long-term investment in partners and supply enterprises.

Non Current Assets– 1.960.892

The 65% of NCA comes from investments in partners and suppliers too, but in this case the investments are in short-term

Equity-Liabilities=3.432.654

Equity- 1.851.248 (54%)

Non Current Liabilities- 855.570 (25%)

Current Liabilities- 725.830 (21%)

Indicators

General Liquidity Radio= 2,03

Acid test= 1,87

General Liquidity Radio is more representative in this case because the inventory is very liquid. It measures the relation between the avaibility of cash in the short term and the cash required in the short term to meet the corresponding debt.

Acc. Payable Period= 57 days

Acc. Receivable Period= 32 days

This is the common situation, because the company must always seek to recover as quickly as possible and pay as late as possible.

Inventory Turnover= 13.9

The inventory is sold many times during the year. This means high efficiency.

Assets Turnover= 0.59

So the efficiency of the company in order to use its assets to generate sales income for the company is low.

Sources:

www.eroski.es

http://www.cnmv.es/AUDITA/2011/13268.pdf

Comentarios desactivados en Eroski financial situation /

30 Nov 2011

por

David Garcia

Sin categoría /

.png)

].gif)

].png)

].png)

].png)

].png)

].png)