On the erroneous belief of understanding the arrival point of development

Diligent students of Economics might wonder what a scene from a Julia Roberts movie and the Italian expression “dolce far niente” have to do with development. Having been an Economics student myself confronted with heavy loads of neoclassical and neoliberalism theory, I would like to shed some light on the coherence of the aforementioned from a new point of view.

When researching definitions of “development”, one encounters numerous versions with rather diverse quintessences. For the purpose of this blog post I would like to concentrate on the following interpretation by the G8 of development as “… a strong, dynamic, open and growing global economy“. This choice is not one taken out of agreement, but one that tries to focus on the pivotal assertion that still drives the development discussion today. It is a discussion that is dominated by only a few parties, namely the Western nations 1, and it is directed if not to a single pathway of development at least to a single arrival point: consumerism. Post-development thinkers, such as Wolfgang Sachs, refer to the 1949 inauguration speech of Harry S. Truman, 33rd President of the United States, as the corner stone of the first world hegemony in development. In this inauguration speech Truman proclaimed:

“[…] we must embark on a bold new program […] for the improvement and growth of underdeveloped areas. […] Their economic life is primitive and stagnant. […] Greater production is the key to prosperity and peace.”

By coining the term “underdeveloped areas”, Truman constructed a hierarchical system that imposed a materialistic Western lifestyle, an “American World Dream”, as the ultimate goal of development on the rest of the world. On the verge of the Cold War, it was a strategic move to demand allegiance of the decolonizing countries of the third world to the first world reinforcing its supremacy against the communist-socialist bloc. US economist W.W. Rostow argued in his 1960 “The Stages of Economic Growth: A Non-Communist Manifesto” that with the right development assistance of capital and technology all countries would eventually converge to the ultimate stage of development, “high mass consumption”, from which the USA had already emerged from.

Largely concealing the fact that this prevailing notion of development is socially constructed and is an ideological concept generating power for the first world, it has found its way into the syllabi of leading universities in the form of varying development theories and it has successfully been perpetuated from there on. As a response to the failure of “improving the life of the masses”, development policies shifted repeatedly during the last 60 years: from growth orientation over poverty alleviation towards the aggressive neo-liberal policies of the Washington Consensus 2 implemented by the Structural Adjustment Programmes by the World Bank and the International Monetary Fund (IMF) in the 1980s, when debt levels and aid-dependency spiked (Moyo, 2010, p. 20-21).

Despite the failure to advance development, it “… had achieved the status of a certainty in the social imaginary” (Escobar,1995, p.5) in such a way that even the opponents of capitalism looked for alternative ways to develop, rather than questioning the construct of development and its arrival point itself. This mistake is equally reflected in the different ways and the evolution of how development has been measured ranging from purely economic indices that depict economic growth (e.g. gross national income per capita, gross domestic product) or defining the percentage of people living below the poverty line 3 to multidimensional indicators of human development such as the New Human Development Index (2010) of the United Nations Development Programme (UNDP). The latter include factors such as life expectancy, birth rates, literacy, years of schooling and income, which again play into the hands of the already known development front runners. Despite the creation of hierarchies and the homogenisation of “under-developed countries”, I believe that the biggest mistake herein lies in the assumption to know the arrival point of development, which in turn leaves little necessity, but also little freedom for the front runners to change.

From a Western perspective, what assures us in the end that we objectively chose the right path to development? Based on national footprint data from the Global Footprint Network, Tim De Chant calculated that at least 4.1 worlds would be needed in order for 7 billion people to live an average American lifestyle 4. Luckily we only have one world. So, if the development myth of the last 60 years neither has worked nor has been proven to be a realistic vision for the entire world at all, has it brought any good for the countries that reached the “top of the ladder”?

Source: Illustration © 2012 Tim De Chant, Data from Global Footprint Network

Aristotle firstly described that happiness (eudaimonia 5) is the ultimate end for all human activities and all activities are therefore only means to pursuing happiness, not ends in themselves. It is enticing to assume that if there could possibly be a universal goal for development, it could only be the pursuit of happiness. Despite the fact that the Unites States had already recognised precisely this as an inalienable right in their Declaration of Independence in 1776, it took over 200 years for happiness to take center stage in the broader discourse about development. In 2006, the New Economics Foundation introduced the Happy Planet Index (HPI), which measures “the extent to which countries deliver long, happy, sustainable lives for the people that live in them”. Four years later, the UN Sustainable Development Solutions Network followed with the first World Happiness Report (2012). Attempting to measure happiness on a global scale, six factors are being used: GDP per capita, healthy years of life expectancy, social support, trust, perceived freedom to make life decisions, and generosity. Critics of the past approaches to development might favour this new course and feel vindicated by the fact that the report highlighted the circumstance that “despite strong economic growth” happiness had stagnated in the USA since the 1950s (Helliwell & Layard & Sachs, 2012, p.61). It would be hypocritical, however, to incautiously declare happiness as the new panacea for development and it might result in making the same mistake this post is trying to highlight in the first place. The following should explain how the newest debate of development is still caught up in its initial mistake.

Source: Happy Planet Index, Map for Experienced Well-Being 6

The initial development debate described high mass consumption as the arrival point of development and with it a set of policies was created by first world countries that allowed for interventions in “poorer countries” that were seldom altruistic. In contrast, the theoretical beauty of defining happiness as the ultimate arrival point of development is that happiness in its philosophical sense is something utterly subjective, a self- determined measure of achieving what one wants in life — whatever that be and by whatever means this can be achieved. But it seems rather naive to believe that the concept of happiness is not strongly subject to ideological contextualisation and that we actually open up the way to a freely open discussion about “development”. I dare to raise the question whether the attempt to measure happiness using constructed proxies such as generosity destroys the exact justification of the pursuit of happiness as the only universally favourable concept of development: subjectivity. Does it not declare the “status of certainty” 7 of just another constructed arrival point of development despite being barely less ideologically biased than the previous development agendas? Is the pursuit of happiness a new “wolf in sheep’s clothing” to perpetuate the hegemony of a few countries?

To refer back to the introduction of this article, I believe that in many Western cultures we are indoctrinated that happiness is achieved by increased economic productivity, efficiency and consumerism. Forced onto society with the help of vast quantities of advertisement, this absolutely fails the liberal definition of happiness, but helps to ensure the economic system from within. By making happiness measurable and comparable, the only thing we achieve is giving a new name to an old strategy.

In the first World Happiness Report of 2012, American Economist Jeffrey Sachs successfully describes the phenomenon of “the ills of modern life” (Helliwell & Layard & Sachs, 2012, p. 3-4) such as obesity, smoking, diabetes and depression and calls them “disorders of development”. The subsequent report in 2013 promisingly even devoted a whole chapter to mental illness “as the main cause of unhappiness”, but I believe that it disappointed in two facts: Firstly, the report states that “…the large majority of persons with a mental disorder reside in low- and middle-income countries of the world” (Helliwell & Layard & Sachs, 2013, p. 41). However, the report then follows with data from the World Health Survey describing depression rates by groups of countries showing the following results: high-income countries 7.1%, upper middle-income 7.6%, lower middle- income 6.4% and low-income 6.0%. It seems that the initial statement is therefore not coherent with the findings of this study, but tries to reinforce the economic hierarchy constructed at the historical beginning of the development debate. My statement should in no way question the existence of equal importance of mental illnesses in the “developing countries”, but rather suggest a perceptual bias in the interpretation. Secondly and most importantly though, the World Happiness Report 2013 defines risk factors for mental illness such as loneliness, bereavement or a low self-esteem. Despite briefly explaining the problem of under-treatment of mental illnesses and introducing effective ways for treatment, the report does not question at all what causes or favours the risk factors of mental illness to originate or to increase. I believe that the World Happiness Report capitulates to the past development approach and does not reflect sufficiently on the possible influence of systemic errors in the contribution to mental illnesses and therefore reduced happiness.

Like other development approaches before, the pursuit of happiness in the ascribed way is looking for remedies to problems that are caused by a system that the approach itself tries to uphold, because dealing with the actual cause of the problem would most likely require a change in that same system. The initial movie scene from “Eat, Pray, Love” should surely not be used as a serious reference, but it puts in a nutshell what from a societal point of view is starting to be recognised in different movements: We live in a world where happiness is imposed to come from economic wealth and in which technology helps us to become more and more efficient and time saving in what we do. But instead of directing this newly achieved time towards things that essentially would make us happy, we use the time to become even more productive and more busy. Sadly, “dolce far niente”, the sweetness of doing nothing, became socially unacceptable in many contexts.

Ultimately, I wonder if followers of movements that try to “slow down life” and reconnect it to real terms can teach us anything about development? The only fact that it can hopefully support is that the assumption to know a generalised ending point of development is an erroneous belief. Or did Rostow actually expect the emergence of a social group that would prefer to be modern traditionalists rather than pure modernists?

1 The “first world” or “the West” describes a group of capitalist countries aligned with the United States after World War II that were opposed to the “second world” communist-socialist countries states headed by the Union of Soviet Socialists Republic. Accordingly, the third world incorporated non-alined states.

2 The Washington Consensus are ten economic policy prescriptions developed by John Williamson that are used for the structural reform of countries in crisis.

3 In the EU the poverty line is defined as 60% of median income.

4 Highest ranked were the United Arab Emirates with an estimate of 5.4 worlds needed.

5 Aristotle described the concept of happiness in the Nicomachean Ethics.

6 Experienced well-being is assessed in the HPI using data from the Gallup World Poll, which asks respondents to imagine a ladder, where 0 represents the worst possible life and 10 the best possible life, and report the step of the ladder they feel they currently stand on.

7 Compare to Escobar, 1995.

References:

De Chant, T. (2012). If the world’s population lived like…. Available: http:// persquaremile.com/2012/08/08/if-the-worlds-population-lived-like/. Last accessed 5th January.

Escobar, A. (1995). Encountering Development: The making and unmaking of the third world. Princeton, New Jersey: Princeton University Press.

European Anti-Poverty Network. (n.d.). Poverty and Inequality in the European Union. Available: http://www.poverty.org.uk/summary/eapn.shtml. Last accessed 4th January 2016.

G8. (2001). G8: The Final Official Notice. Available: http://www.un.org/esa/ffd/themes/ g8-5.htm. Last accessed 3rd Jan, 2016.

Jefferson, T. (1776). The Declaration of Independence. Available: http://www.ushistory.org/ declaration/document/rough.htm. Last accessed 5th January.

Helliwell, J & Layard, R & Sachs, J (eds.). (2012). World Happiness Report. New York: The Earth Institute, Columbia University.

Helliwell, J & Layard, R & Sachs, J (eds.). (2013). World Happiness Report 2013. New York: UN Sustainable Development Solutions Network.

Helliwell, J & Layard, R & Sachs, J (eds.). (2015). World Happiness Report 2015. New York: Sustainable Development Solutions Network.

Moyo, D. (2010). Dead Aid: Why aid is not working and how there is another way for Africa. London: Penguin Books.

Rostow, W W. (1960). The Stages of Economic Growth: A Non-Communist Manifesto. 3rd ed. Cambridge: Cambridge University Press.

Sachs, W. (2010). The Development Dictionary: A Guide to Knowledge as Power. 2nd ed. London: Zed Books.

Taylor, C. (2006). Aristotle: Nicomachean Ethics: Books II-IV. Oxford: Oxford University Press.

The New Economics Foundation. (2006). The Happy Planet Index. Available: http://www.happyplanetindex.org. Last accessed 8th Jan 2016.

Todaro, M & Smith, S. (2012). Economic Development. 11th ed. Boston: Pearson Education.

Truman, H. (1949). Inaugural Address. Available: http://www.presidency.ucsb.edu/ws/? pid=13282. Last accessed 3rd Jan, 2016.

Enviar comentario /

11 Jan 2016

por

Judith Spring

IMSD /

IMSD /

How motivated people create -a real- change

Ever since I started my business degree in college our professors tried to shape our mindsets under the dogma for which Michael Porter jumped into the “hall of fame” of the Harvard academics: Strategy is War. You have to squeeze your suppliers, create barriers for others to enter the market and defeat your competitors if you want to get somewhere in business.

But I wanted to create love, not war –also Michael Porter got to this conclusion after 30 years-. But, how a person could shape the future creating a positive impact and make a living at the same time?

The answer is being a social entrepreneur (or intrapreneur). These are brave, transgressor, nonconformist and brilliant people whose favorite prefix is “co-“: co-work, co-exist, co-create… collaborate at last (this last one without prefix).

The real changemakers for who the CSR policies are ok but definitely not enough because their passion for making social change is the fuel of their businesses.

“I don’t believe in charity. I believe in solidarity. Charity is so vertical. It goes from the top to the bottom. Solidarity is horizontal. It respects the other person. I have a lot to learn from other people.”― Eduardo Galeano

This new business concept reshapes any statement any MBA has ever learned because, stepping out from philanthropy, social entrepreneurs identifies a social problem that can be alleviated through a venture that generates profits at the same time it creates social change.

But, if the social motive was not inspiring enough, I find in motivation the key of their success. How motivated people can create –a real and tangible- change can be clearly seen in social INTRApreneurs: people who work for corporations and create change from within, because their passion and motivation drags people around and are able to shake the pillars of any organization.

And you, do you thank God because its Friday or because its Monday?

Enviar comentario /

12 May 2017

por

Cristina Kirkendall

IMSD /

Stepping Away from the Dark Side: A New Hope

I have been hearing a lot about sustainability in the banking sector but when I personally think about banks I think about the opposite. I think about speculation and financialising in which the traditional principles of a are far from gone. No longer do banks invest in small business owners and other local businesses but instead the savings of people like you and I are used in endless speculation and investments we know nothing about.

Never before have I personally considered what my bank was using my money for but something made me think. Being a sustainable development student I want those few pennies that I have to be invested in projects/businesses/funds which I personally feel good about.

Recently most banks are beginning to claim that they want to be a part in making the economy and society more sustainable.

This could mean that the values of the traditional banks suddenly changed and that they genuinely want to change the way of conducting business, but unfortunately I believe it is much more likely this is another convenient way of greenwashing. Because understandably it is very likely that most of the banks customers won’t be checking their banks financial activities anyway.

This could mean that the values of the traditional banks suddenly changed and that they genuinely want to change the way of conducting business, but unfortunately I believe it is much more likely this is another convenient way of greenwashing. Because understandably it is very likely that most of the banks customers won’t be checking their banks financial activities anyway.

But although I don’t trust these conventional banks claiming they strive for sustainability, I do believe there is hope and that there is no future for conventional banks if they don’t really, truly, honestly, transparently, openly change. As with all transitions there needs to be leaders and although I am aware that there are more examples of sustainable banks I want to focus on Triodos bank. Triodos bank functions like any other conventional bank except for one very important difference, Triodos bank only invests in sustainable businesses. Where conventional banks promise low risks and high returns a bank like Triodos adds an aspect which is impact. This means that the investments made and the funds that they offer strive for positive impacts in the world.

When learning more about Triodos I actually opened a bank account immediately because I truly believe there is a future in impact investing and a sustainable banking world. Maybe because I am in contact with sustainability everyday due to my master course it is more likely that I open a sustainable bank account than others but I think there is a transition happening. So let me end my post with a very opportunistic future projection: I project that in the near future the conventional banks will die out or need to transition and there will be a new era of more sustainable banks. If the financial world can make this step everything is possible and we might even live to see a better greener world.

Yours truly,

Tim Wierks

Enviar comentario /

12 May 2017

por

Tim Wierks

IMSD /

Money as a change driver

In a fast growing and every time more interconnected world, capitals move all around and is interesting to see how this investing practices have been changing moving from traditional schemes where the only goal was to have the highest return without considering how it was achieved, into a new growing market where investor are finding interesting and profitable to invest in projects focused in solving environmental and social issues.

Two new ¨investing¨ modalities are gaining relevance and spreading through different markets and countries. One is known as impact investment and the other one is call Venture Philanthropy. Even though both have the same target of allocating resources for projects that solve environmental and social issues, both do it using different tools and expecting different monetary results.

Venture Philanthropy it is a small but growing field which main purpose is to take the tools and mechanisms used in regular ventures, and put them in practice to promote non-profit organizations, sustainable star-ups and risk-taking social ventures, which usually struggle to get funds from the traditional financial services.

This type of investment is known by the close attachment of the philanthropist and the social entrepreneur or the area of research he/she is developing. In most of cases are investments with no expectation of financial return or it could be non-financial support like knowledge transfer, networks or coaching. In both cases, there are areas of potential improvement about the measurement of results or achievements made during the project since the main way to evaluate the success is the impact achieved.

A clear example is Ashoka and organization through which philanthropist (mainly private companies and investors) donate money to it and then is in charge of looking for the most drive changers social entrepreneurs all around the world to promote their projects and like this promote a social change.

On the other hand, we find the Impact Investors, that like the venture philanthropist are looking to achieve through their

On the other hand, we find the Impact Investors, that like the venture philanthropist are looking to achieve through their investment, is to promote projects that pursue social and environmental impact but the big difference is that they are actually looking for a financial return that could be below, equal or higher than value markets and because of this, the impact measurement takes relevance for the investor in order to guarantee that financial, social en environmental targets are being accomplished compared to the one settled at the beginning of the project.

investment, is to promote projects that pursue social and environmental impact but the big difference is that they are actually looking for a financial return that could be below, equal or higher than value markets and because of this, the impact measurement takes relevance for the investor in order to guarantee that financial, social en environmental targets are being accomplished compared to the one settled at the beginning of the project.

Impact investment is spreading every time more along different sector and institutions like banks, pension funds, family foundations and government institutions achieving by 2015 $15 billion in impact investment and for 2016 $17,7 billions and for what could be seen in the graphics, most of the investors interviewed revealed that the returns obtained are the expected one which will be an incentive for this type of investments.

There are still challenges that this tow type of investment face must towards the future panorama i n order to become star products. Some of these are: the implementation of more elaborated indicators to evaluate the social and environmental impact, innovation in the product structure to reach a bigger number of investors, bring accurate information about this kind of investment to become a more attractive alternative in the market and government support to the sector.

n order to become star products. Some of these are: the implementation of more elaborated indicators to evaluate the social and environmental impact, innovation in the product structure to reach a bigger number of investors, bring accurate information about this kind of investment to become a more attractive alternative in the market and government support to the sector.

Bibliography:

https://thegiin.org/impact-investing/need-to-know/#s2

Enviar comentario /

12 May 2017

por

sgonzalezmoreno

IMSD /

Social Entrepreneurship: Changing Mindsets

“There is no greater disability in society than the inability to see a person as more”

– Robert M. Hensel

Having always struggled with concentration and keeping my mind on the task at hand, I have worked hard to implement methodologies into my daily life to maintain my attentiveness. Despite my efforts, I find myself getting up from chair every five minutes whilst writing this blog. Without even realising I have moved from my desk and entered the kitchen to start cooking dinner, followed by me leaving the vegetables half prepared as I remembered I was supposed to call my mum two days ago.

My Masters is a small class of 11 students, and over the past 7 months we have gotten to know each other well. Even so, it took me by surprise when a class mate was able to observe my behaviour and question if I have an attention deficit disorder. Prior to my masters course I would have taken this as a negative comment, but was relieved by their assurance that regardless of having these characteristics they are not a hindrance to success.

The Social Entrepreneurship lectures of my course have delved into the world of the Ashoka organisation, providing a breath of fresh air. The foundation is focused on supporting change makers across a range of projects, all striving to tackle and overcome social, environmental or cultural issues using innovative and original methodologies. Ashoka offers a small financial injection but mostly provides benefit through the use of their platform which encourages details of the projects to spread and grow.

They back a range of carefully selected “fellows” who must adhere to a list of five key characteristics:

- New and innovative idea to a social problem

- Creativity in the solutions

- Positive Social Impact of the idea

- Entrepreneurial Quality

- Ethical Fibre of the Entrepreneur

One story which particularly resonated with me was the project of Danish innovator Thorkil Sonne who founded the Specialist People Foundation. This foundation has created pathways to meaningful employment for over 1 million people worldwide. Sonne was able to take the characteristics associated with Autism which are usually seen as a disability, and therefore disadvantageous, but pivot by identifying major strengths and potential competitive advantages for businesses. Intertwined with the daily challenges faced by autistic people there is an attention to detail, precision and absolute focus that complements working in high-skilled analytical jobs. He was therefore able to flip societies thinking about disabilities and employability.

By providing suitable working environments and a space to develop and capitalise upon their skill sets, each person finding work through this foundation is empowered to focus on their diverse and vast set of capabilities and escape the label of having a “disability”.

Following on with the theme of flipping the way we think, the work of Narayana Peesapaty creating edible cutlery was a complete revelation for me. On a myriad of occasions; especially since moving to Madrid which is a city prone to good weather, I have attended picnics or BBQs supplied with one-time use plastic cutlery, which simply gets thrown to the rubbish. This is totally unsustainable process but through the introduction of this alternative option, which reverses our way of thinking, both people and the environment can be benefited. Eat with it and then eat it.

Resources

https://www.ashoka.org/en/engage

https://www.ashoka.org/en/fellow/thorkil-sonne

http://www.bakeys.com/profile-of-the-founder/

http://www.doctorsintraining.com/blog/positive-affirmations-for-usmle-board-preparations/

Enviar comentario /

12 May 2017

por

jyoung

IMSD /

Co-creating solutions. Welcome to the era of collaboration

In a world defined by rapid change, the need for innovative solutions to social and environmental challenges has become more complex, market systems have become interconnected and public policy and industry norms are not changing as fast as it is needed.

Here is where the idea of co-creating solutions and collaboration pops up, we are moving from a traditional competitive world to a cooperative and collaborative world to be able to find effective and innovative solutions for the problems or challenges.

Cooperation is the trend nowadays, we start with co-working spaces where people can share their ideas, being The impact hub Madrid a perfect example of this spirit of cooperation and co-creation of solutions. Impact Hub offers a unique ecosystem of resources, inspiration, and collaboration opportunities to grow the positive impact of your work.

Showing that co-creating ideas and cooperating with other people can be the perfect combination to reach our goals, help the society, have a meaningful project and why not have a good time while doing it.

Co-creating solutions a revolutionary way of thinking where we are evolving the mindsets of the people, companies and organisations in general, thus here is where the social entrepreneurs appear.

What distinguishes entrepreneurs from everyone else is that their job is to change the overall patterns and systems of society. Can there be anything more impactful than a global team of the world’s best entrepreneurs who develop a strategy to tip the world toward a better future?

Social entrepreneurs are the main defenders and the soul of the idea of co-creating solutions and cooperation.

That is the good thing about co-creating solutions you just have to put your small idea within other people and you could or not become bigger with the ideas of other entrepreneurs but that is the beautiful thing about that.

A perfect example can be the founders of ClickMedix and DC Greens that combined forces and launched an innovative project based on a mobile app and digital platform that allows low-income, Washington, DC residents to redeem vouchers prescribed by doctors for fruits and vegetables at local farmers’ markets. As they say in an Ashoka´s article in Forbes “This is a tale of the power of collaboration – of what happens when two smart, passionate and committed women who are trying to change the world around health access get real and unguarded about their business challenges and build together in the spirit of community and sisterhood”.

Besides, co-creating solutions are not only for social entrepreneurs but also can be a very good method for companies or organisations among others to become successful and contribute with the world and with others at the same time that they go for their own objectives.

Another co-creating solution project is:

“I-nnovate for Tomorrow”: Co-creating Solutions together with the Sudanese Children

UNICEF Sudan together with UNICEF’s Child Protection and Education sections organised a national youth workshop called “I-nnovate for Tomorrow” in which young people are tasks to help design recreational kits that suit children’s needs in Child-Friendly Spaces (CFS).

But one of my favourites examples is the collaboration between the so-called competitors: Harvard and MIT creating the edX. Harvard University and Massachusetts Institute of Technology (MIT) have signed an agreement to create EDX, a non-profit organisation that aims to offer free online courses, adapted from traditional courses to anyone with an Internet connection. edX is designed not only to build an online global community of students but also to investigate new learning methods and technologies

I can be naming examples the whole day but I think the idea is crystal clear: co-creating solutions and collaborating is the new trend and the new solution to challenges.

At the end co-creating solutions is an effective way of facing the new challenges that we have nowadays, the new era of cooperation needs solutions to fulfil these new expectations and social entrepreneurs collaborating with companies can be the ones in charge of continuing and leading this. Collaboration does not need to be an enemy of innovation, speed or profitability.

As Ashoka said “The parallel efforts of hundreds of entrepreneurs, civil sector organisations, businesses and other stakeholders can be joined and multiplied without impeding the work of any individual actor. Indeed, in a world whose problems escalate every day, there may be no other solution”

PS: Check also the wonderful collaboration between Corporación Sanitaria Parc Taulí de Sabadell + BVentura or Kalundborg Symbiosis: A cooperative circuit for recycling and reuse of industrial waste

1 comentario /

12 May 2017

por

lsastreestevez

IMSD /

The new type of philanthropist

According to the CAF (Charities Aid Foundation) World Giving Index the world is becoming more and more generous. This organization has been measuring monetary donations, volunteering time and indexes of helping a stranger in 140 countries for 7 years. Just the United Stated alone donated $373.25 billion dollars in 2015, the most generous year ever (no records of 2016).

When we talk about philanthropy it is important to have in mind that we are not talking just about money, people can help in many ways to a good cause: expertise, time, experience, tools, resources, etc. Because even though money can help a lot it is not always a solution. In certain occasions it may solve the problem in the short term, but acts like a barrier for the long run. If philanthropy is addressed this way we can say that it “targets symptoms, not causes”.

I don’t believe that philanthropic aid is enough to solve the social problems we face nowadays, but it can help to reduce it temporarily. I still think that small changes and contributions can have a big impact and as a community we should help those in need. It is important to keep in mind to always have a global and complete solution with a long term vision.

But what happens when donations end? What if all the donors demand results? Or want to get more involved?

The good news is that there is a new way to help social problems, make money, have long term vision and impact others an it`s called social entrepreneurship. This new way of making business changes problems for opportunities.

The main difference between philanthropy and social entrepreneurship is that this last one aims to be sustainable, empower individuals, re-distribute profit, solve problems with innovation, partner with allies and collaborate with people that are looking for the same objective. I like the vision form Skoll Foundation were they define it as:

“Applying business skills to solve social ills” & “Betting on good people doing good things”.

For example when Bridget Hilton learned that according to the World Health Organization and the UNICEF more than 5,000 children die every day from diseases that could have been avoided by simply washing their hands, she was deeply moved and decided to found Hand in Hand. This company sells soaps in the US and donates one to a child in need. To ensure that the project has a real impact and good hygienic practices continue, Hand in Hand gives workshops to promote this and creates partnerships with local NGOs.

Right now there is a trend that is helping social entrepreneurs: associations like Ashoca or Skoll Foundation that support all this kind of projects, people and companies that want to make Social Responsible Investments, donators that want more results and sustainable projects in time with profits that can be reinvested. Is the opportunity to think out of the box to solve social problems.

I found refreshing this new proposal. It makes me have hope that there are people with creative solutions that can have a real impact in the social issues we face nowadays and at the same time have profits that can be reinvested and help more and more people.

Enviar comentario /

11 May 2017

por

aespana

IMSD /

Social intrapreneurship as CSR solution:

The social entrepreneurship movement is focus in offer innovative solutions for the global problems that affect to the society, offering creative products or services that create a positive impact. Since the appearance of the movement it has increased a lot the number of new enterprises that have applied the start-up model to address social issues, looking for a sustainable manner to maintain the mission of the company in the time.

Wherever, sometimes these enterprises needs a initial capital that finance the beginning of the company, its profits are reduce to maintain the activity of the company, which can drive to the owner of the company to a difficult situation due the high amount of resources needed if there is no solvency for the sustainability of the enterprise.

An innovative approach that can help to solve this issues is the social intrapreneurship, which are social entrepreneurship initiatives created inside of the company by their employees. This initiatives can take advantage from the logistic already establish of the company, which also gives some financial and marketing support.

Social Intrapreneurship.

An example of social intrapreneurship, is the one created by Graham Simpson, from the multinational GSK. While on a six-month placement in Kenya, he was struck by people dying from easily treatable diseases mainly through the lack of effective diagnosis. So he decided to develop the idea of developing cheap, yet commercial, diagnostics kits that could be used by often health workers in rural villages, sometimes far away from hospitals. GSK is now working with John Hopkins University to develop the kits.

GSK Social Intrapreneurship Iniciative.

The expected impact of the social intrapreneurship can be huge, According to an Accenture report: “More than 50% of the 100 largest economies in the world are companies. A minimal change made from the bottom up by a social intrapreneur can make a big difference for the communities reached by these same companies” (1).

If Social intrapreneurship is well managed, it can be converted in a powerful tool for the companies, getting at the same time the possibility to engaged motivated employees at the same time that can help to develop the corporate social responsibility policy of the company. With those types of initiatives, companies would contribute to the environment and society issues without affect to their economic accounts or a mayor effort by their side, which can drive them to start moving towards sustainability.

(1). https://www.changemakers.com/es/blog/intraemprendedores-sociales-innovaci%C3%B3n-desde-las-empres

(2) https://www.theguardian.com/social-enterprise-network/small-business-blog/2013/apr/17/social-intrapreneurs-changemakers-companies

Enviar comentario /

11 May 2017

por

arodriguezbolanos

IMSD /

Asking myself where the limits were.

Social entrepreneurs are all those entrepreneurs with the capacity of detecting social or environmental problems that could be solved from a creative and innovative approach, getting to the solution with their multitasking skills. Tough work. Different from these brave people, are the “interpreneurs” being not more, not less, but different kind of change makers. What interpreneurs do is basically practice entrepreneurship within large corporations.

With this new figure in my mind, and in the middle of a complex job-searching phase, I came up to wonder myself about where were the limits between doing a genuine work versus doing a green washing work when making correct social-environmental actions at one of those large companies that produce more negative impacts than positive ones.

Although the communication of the corporation’s ethical actions to investors, final consumers and any other stakeholder is done through the Sustainability Report, sometimes is difficult to truly believe and see if the company is doing the right thing. So, when I imagined myself working in that side of the coin, more and more doubts kept coming to my mind… How people would perceive it? Are this works enough? What weights more?

I do not have all those answers. Nevertheless, with some help of my mentor in this subjects, I arrived to one that I´d like to share: the main driver to get the personal values, achieve the company´s goals and comply the stakeholder´s expectations probably is doing what we love the most: Doing the right thing.

Being empathic, innovative, passionate.

Detecting urgent problems, using the capability of the company, and solving them with our capacities.

Being the example for the others.

Doing what is the best for the society and the environment.

Being and inspiration for our circle of influence.

Being sustainable.

Being a change-maker.

And last but not least…

If we want to change the world, we will have to be surrounded with others that want to change the world too. Because change IS possible, and older IMSDs have shown it.

So, my advice to me and to the others is: Just be the change we want to see in the world (Ghandi).

I´m sure we will make it.

Best regards!

Julieta

Enviar comentario /

11 May 2017

por

jpezzutti

IMSD /

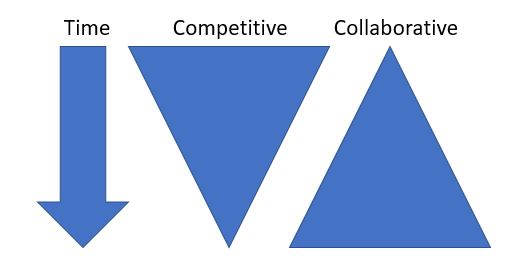

The Shift from Competition to Collaboration

I went to business school for my undergraduate degree, so I will always remember Porter’s 5 forces. The 5 forces have been taught as business strategy since the 1980’s. This framework is rooted in competition, as it determines the level of competition or rivalry within a given industry, and that competitive understanding provides the basis of the business strategy. This has been the status quo for so long, so many businesses today have strategies that are competitive at the core.

I went to business school for my undergraduate degree, so I will always remember Porter’s 5 forces. The 5 forces have been taught as business strategy since the 1980’s. This framework is rooted in competition, as it determines the level of competition or rivalry within a given industry, and that competitive understanding provides the basis of the business strategy. This has been the status quo for so long, so many businesses today have strategies that are competitive at the core.

In a world that is changing faster than we can keep up with, some businesses rooted in this competitive framework may not be able to adapt. For example, Porter’s 5 forces provide framework for being competitive within a stable industry. What happens when technological advancements and innovation create whole new industries, or completely flip existing industries? It’s hard to apply this competitive framework, especially when emerging industries and businesses are starting to become part of shared economies and more collaborative in nature.

This simple graphic shows the shift from competitive strategies to collaborative strategies that we will experience as we head into the future.

Take the example of rides for hire. The status quo was a taxi or personal driver. A taxi company rooted in competitive strategy would have likely had a business strategy focused on providing the best cars with the best drivers to create an advantage. But as we have moved to a shared economy, collaborative businesses such as Uber or BlaBlaCar have emerged and completely flipped the industry. Uber has even started partnering with other industries, such as food delivery, to create services like UberEats. This service goes beyond rides for hire and collaborates with an entirely different industry – the restaurant industry. And, unfortunately, many taxi companies that have not been able to adapt have been left behind during this shift.

What is exciting about this trend is that it opens up many opportunities for social entrepreneurs and enterprises to excel. This is because social enterprises are collaborative in nature, as they need support from many business, influencers, and stakeholders around them, and social enterprises collaborate with their targets and their stakeholders from the enterprise’s inception. When a social entrepreneur has an idea to make a positive impact in the world, the idea often needs support from people with additional talents to support the business, social influencers to market the business, and partners with capital to succeed. Because social enterprises provide net benefits for so many stakeholders and the community, the help given from those that support the enterprise is often reciprocated in some way, furthering the necessity and benefits of collaboration.

One example of a highly collaborative social enterprise is WeShareSolar, from the Netherlands. The name of the company itself even implies collaboration. This project solves a green energy transition problem in the Netherlands: installing solar panels at home or for small community projects has a financing gap, as the projects are too small to receive bank lending, but the costs are too high for residents or communities to finance themselves. Furthermore, many residents (43%) don’t have access to a sunny roof in order to consider installing a solar panel. WeShareSolar provides a highly collaborative solution – it uses crowdfunding to invest in solar projects, and once the solar projects are financed and eventually built, the solar power can be distributed to the grid, therefore providing energy savings to many more people and communities, as well as net environmental benefits by reducing carbon emissions.

WeShareSolar involves many stakeholders in a collaborative way: those wanting solar power but don’t have roofs or cannot afford the panels can still donate via crowdfunding, and wind up receiving the savings produced by solar power. Crowdfunders can start their investment with as little as €25, and they make an annual return of 3-6%. For larger projects, WeShareSolar works alongside banks, making solar power for larger buildings or businesses more affordable. Since this business model is scalable, it can be applied to other industries as well. The model can also be replicated in other countries, particularly developing countries, that rely more on solar to increase energy access. Finally, to date, WeShareSolar has already saved 470,000 kg of CO2.

This example embodies the shift from competition to collaboration. Crowdfunding combines financing from many individuals in order to provide a communal service that provides energy savings in the end – a perfect example of a shared economy. Additionally, with a competitive business strategy, banks could have been seen as a main competitor. However, WeShareSolar has found a way to work with banks to scale their offerings, all while providing a net benefit of energy savings and reduced CO2 emissions in the end. By putting collaboration at the core of the business strategy, WeShareSolar has been recognized as a Lighthouse Activity by the UN and has grown into the largest solar crowdfunding platform in the EU.

Sources:

http://unfccc.int/secretariat/momentum_for_change/items/9929.php

https://www.zonnepanelendelen.nl/

Enviar comentario /

11 May 2017

por

Ashley Hodges

IMSD /

Systemic changes are being accomplished by social entrepreneurs

“And above all, watch with glittering eyes the whole world around you because the greatest secrets are always hidden in the most unlikely places. Those who don’t believe in magic will never find it.” ― Roald Dahl

The traditional way of entrepreneurial ‘forces for good’ has been embedded in the idea of entrepreneurs that accumulated wealth in the private sector, and becoming philanthropists later in life. Bill Gates and Warren Buffet are among the world’s most famous philanthropists. Together they have donated over 60 billion dollars in causes such as health care, extreme poverty, and education.

By the end of the end of the 70s of the last century, a new force for good emerged with the advent of Bill Drayton who founded Ashoka. An organization that fosters and stimulates entrepreneurs who work towards positive (social) change, through their core businesses. A new business model has emerged: social entrepreneurship.

Social entrepreneurs have an idea to change the world. They have the ability to see the world differently. They see opportunities where others see problems. They show the world solutions. Mohammed Yunes is a perfect example of a social entrepreneur that changed the status quo by opening a financial market at the bottom of the pyramid through a micro-credit system. Social entrepreneurs create frameworks within a field in order to change it.

“Social entrepreneurs are not content with giving people fish or teaching people how to fish. They will not rest until they have revolutionized the fishing industry” – Bill Drayton

One of Bill Draytons visions on social entrepreneurship, still the vision of Ashoka, is the aim for system changes. ‘Aim for a system change, or the symptoms will just reappear’. Try to reach the ‘tipping point’, where, if you stop operating, the change will still be there. If Mohammed Yunus decides to close the Grameen bank and not operate in micro credit finance anymore, it will not disappear. Microcredit finance is here to stay.

Enviar comentario /

11 May 2017

por

easbeck

IMSD /

.png)

].gif)

].png)

].png)

].png)

].png)

].png)